Table of Contents

Hidden Mutual Fund Fees — The Silent Wealth Killers

Let me tell you something that most mutual fund advertisements will never say out loud.

You can do everything right — start your SIP early, pick a decent fund, stay invested for 15-20 years — and still end up with lakhs less than you expected. Not because markets underperformed. Not because you made bad fund choices. But because hidden mutual fund fees were quietly eating into your returns every single year without you even realising it.

I have seen this happen to genuinely hardworking investors. They invest ₹5,000 a month faithfully for 20 years, and when they finally check their corpus, the number feels disappointingly lower than what any online SIP calculator showed them. The reason is almost always the same — costs they never tracked.

Here is the uncomfortable truth: even a 1 to 2% annual fee looks harmless on paper but can wipe out ₹15-20 lakh from your final corpus over a 20-year SIP. That is not a rounding error. That is a significant chunk of wealth that could have funded your child’s education or your retirement.

In this article, I am going to walk you through all 7 hidden mutual fund fees that investors in India commonly overlook — in plain, honest language — and show you exactly how to protect yourself from each one.

What Are Mutual Fund Fees Exactly?

Before I get into the specific hidden mutual fund fees, let me quickly establish something important.

Mutual funds are not free. They never were.

When you invest in a mutual fund, a team of fund managers, analysts, compliance officers, and support staff is working behind the scenes to manage your money. That team costs money. The AMC (Asset Management Company) needs to recover those costs — and they do so through a variety of charges. Some of these charges are clearly disclosed. Others are baked so quietly into the daily NAV (Net Asset Value) that most investors never see them as a separate deduction.

Here is the simple difference:

Visible charges — Exit load (you see this when redeeming), STT on redemption, platform charges.

Invisible charges — Expense ratio (deducted daily from NAV), distributor commission (hidden inside Regular Plans), portfolio turnover costs (absorbed inside the fund).

Think of it like this. You deposit ₹10,000 into a mutual fund. The fund earns 12% that year. But by the time the gains show up in your account as NAV appreciation, the expense ratio, turnover costs, and distributor commission have already been quietly deducted. You see only 10.5% or 10% — and you assume that is the market return, not realising 1.5-2% has already been skimmed off.

This is exactly why understanding hidden mutual fund fees is so critical for every SIP investor in India.

1) Expense Ratio: The Biggest Hidden Mutual Fund Fee

The expense ratio is the mother of all hidden mutual fund fees and the one that matters most over the long run.

Every mutual fund scheme has an annual expense ratio — expressed as a percentage of your investment — that covers the fund’s management costs. For example, if a fund has a 1.5% expense ratio and you have ₹1 lakh invested, the fund deducts ₹1,500 per year from your investment.

What makes this particularly sneaky is how it is deducted. The AMC does not send you a bill or show a separate deduction line item. Instead, the expense ratio is deducted daily from the fund’s NAV. So if the fund earns 12% gross but has a 1.5% expense ratio, you see a NAV growth of only 10.5%. The cost is invisible in your day-to-day experience.

Active Funds vs Index Funds — The Expense Ratio Gap Is Massive

| Fund Type | Typical Expense Ratio (Direct) |

|---|---|

| Actively Managed Equity Fund | 0.5% to 1.2% |

| Index Fund (Nifty 50) | 0.1% to 0.2% |

| Small Cap Fund | 0.6% to 1.5% |

| International Fund | 0.8% to 1.8% |

| Regular Plan (any category) | Add 0.5-1% extra |

The Long-Term Damage of High Expense Ratio

Here is where it gets really eye-opening. Let us compare two identical investments over 20 years:

- Fund A: 12% gross return, 1.5% expense ratio → 10.5% net return

- Fund B: 12% gross return, 0.3% expense ratio → 11.7% net return

On a ₹5,000 monthly SIP over 20 years:

- Fund A (10.5% net): ₹40.6 lakh

- Fund B (11.7% net): ₹49.8 lakh

That ₹9.2 lakh difference is purely due to the expense ratio gap. Both funds earned the same gross return. The only difference was how much was charged.

My honest opinion: The first thing I check before recommending any fund is the expense ratio. Everything else is secondary. A fund that earns 14% but charges 1.8% will often underperform a fund that earns 12% and charges 0.2% — over a long enough period.

Always choose Direct Plans to access the lower expense ratio version of any fund.

2) Regular Plan Commission: The Fee You Never Agreed To

This is the one that makes me genuinely frustrated on behalf of new investors in India.

When most people first buy a mutual fund — through a bank, insurance agent, or financial advisor — they almost always end up in a Regular Plan. Nobody explains to them that there is a cheaper alternative called a Direct Plan of the exact same fund.

The difference? In a Regular Plan, the AMC pays a recurring commission of 0.5% to 1% per year to the distributor (the bank, agent, or platform that sold you the policy). That commission comes directly out of your returns — not from the distributor’s pocket.

Direct vs Regular Plan — Real Wealth Difference

Let us say you invest ₹5,000/month for 20 years in an HDFC Mid Cap Fund:

| Plan | Expense Ratio | Returns After 20 Years |

|---|---|---|

| Regular Plan | ~1.75% | ~₹47 lakh |

| Direct Plan | ~0.75% | ~₹57 lakh |

Difference: ₹10 lakh — paid to a distributor as commission, silently deducted over 20 years from your investment without your explicit knowledge.

The distributor typically does nothing for this commission after the initial sale. You do all the work of staying invested. They earn money every single year just because you did not know Direct Plans existed.

How to switch: You can buy Direct Plans on platforms like Zerodha Coin, Groww (select Direct), MF Central, or directly on the AMC’s official website. For SEBI’s official guidance on direct vs regular plans, visit https://www.sebi.gov.in.

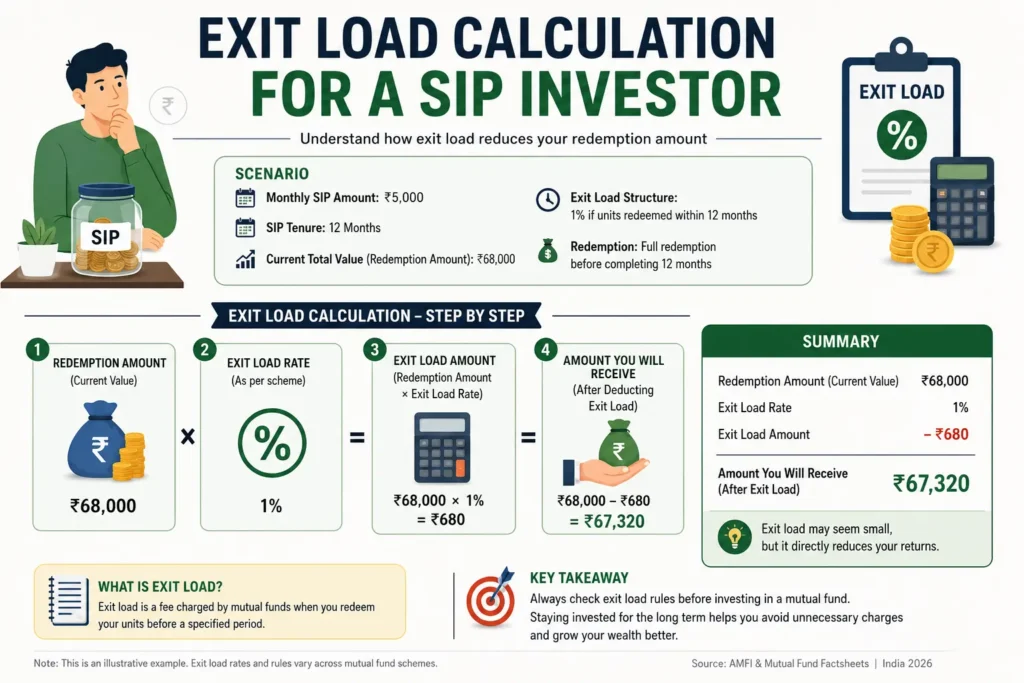

3) Exit Load: The Penalty for Leaving Early

Exit load is one of the more visible hidden mutual fund fees — but investors still get caught off guard by it constantly, especially with SIP redemptions.

Exit load is a fee charged by the AMC when you redeem (withdraw) your mutual fund units before a specified holding period. For most equity mutual funds, this is:

1% of the redemption amount if you exit within 1 year of investment

It sounds small. But let us make it real.

If you invested ₹1 lakh in a mutual fund and you need to withdraw after 10 months — you pay a ₹1,000 exit load instantly. That is money gone before the transaction even settles.

For SIP investors, exit load works on a FIFO (First In, First Out) basis. Your oldest SIP units are redeemed first. If those are more than 1 year old, no exit load. But if you also have units less than 1 year old — which you almost always will in an ongoing SIP — those will attract the 1% charge.

How to avoid exit load:

- Plan withdrawals carefully. Wait until units are at least 1 year old before redeeming

- Use a SIP calculator to track the 1-year mark for each instalment

- For goal-based investing, set your SIP end date 1 year before you actually need the money

4) Securities Transaction Tax (STT)

Most SIP investors have never even heard of STT — which makes it a genuinely hidden mutual fund fee.

STT (Securities Transaction Tax) is a government tax applied when you redeem equity mutual fund units. Currently, STT on equity mutual fund redemption is 0.001% of the redemption amount.

At 0.001%, it sounds almost negligible. On a ₹10 lakh redemption, it works out to ₹100.

By itself, STT is not a major concern. But if you are an investor who switches funds frequently, or someone who makes partial withdrawals regularly from an equity portfolio, STT adds up across multiple transactions and quietly reduces your net proceeds each time.

Key point: STT applies only on equity and equity-oriented hybrid funds during redemption. Debt funds are exempt from STT. The tax is automatically deducted by your broker or platform — you never need to pay it separately, but you also often do not notice it happening.

5) Portfolio Turnover Costs

This is probably the least-discussed of all hidden mutual fund fees — and yet it can be surprisingly significant for actively managed funds.

Portfolio turnover refers to how frequently a fund buys and sells stocks within its portfolio. A turnover ratio of 100% means the fund replaced its entire portfolio once in a year. A ratio of 50% means half the portfolio was replaced.

Every time the fund manager buys or sells a stock, the fund pays brokerage and exchange transaction costs. These costs are absorbed inside the fund itself — they are not shown separately and are not included in the expense ratio disclosure.

Active funds with high turnover ratios (50% to 150%+) silently bear higher transaction costs than passive index funds (which rarely trade at all).

The Index Fund Advantage:

Index funds like UTI Nifty 50 or Nippon India Index Fund barely trade — they only rebalance when the index composition changes, which happens rarely. Their portfolio turnover costs are near zero.

Active funds that trade frequently pay real money in brokerage on every transaction — and that money comes from the fund’s corpus, reducing your net returns.

This is another reason why low-turnover, long-horizon active funds and index funds tend to deliver better net returns than high-activity trading-style funds.

6) Tax on Capital Gains

Tax is not a “fee” charged by the AMC — but it absolutely qualifies as a hidden mutual fund cost that reduces your final take-home wealth. And most investors dramatically underestimate how much tax they will pay on their mutual fund gains.

Here is the current tax structure (as of 2026):

Equity Mutual Funds (including ELSS, Mid Cap, Flexi Cap, Index Funds):

| Holding Period | Tax Type | Tax Rate |

|---|---|---|

| Less than 1 year | STCG (Short-Term Capital Gains) | 20% |

| More than 1 year | LTCG (Long-Term Capital Gains) | 12.5% (above ₹1.25 lakh gains) |

Debt Mutual Funds:

After the Finance Act 2023 removed indexation benefits for debt funds, all debt fund gains are now added to your income and taxed at your applicable slab rate — regardless of holding period. This significantly reduced the tax advantage of debt funds for investors in higher tax brackets.

Dividend Tax:

If you choose the Dividend (IDCW) option instead of Growth option in any mutual fund, dividends are added to your income and taxed at your slab rate (up to 30% for high earners). This is why most financial advisors recommend the Growth option for all long-term SIP investments.

The Tax-Efficient Strategy:

- Always choose the Growth option, not IDCW/Dividend

- Hold equity funds for more than 1 year to qualify for LTCG (12.5% instead of 20%)

- For LTCG above ₹1.25 lakh per year, consider staggering redemptions across financial years to stay under the threshold

- For tax-saving investment, use ELSS funds which qualify for Section 80C deduction

For the most current tax rules, always verify at https://www.incometax.gov.in.

7) Advisory and Platform Charges

The final category of hidden mutual fund fees is one that has grown significantly as India’s fintech ecosystem has exploded.

Many “free” investment apps and platforms earn money in ways that are not immediately obvious to users:

Trail Commission on Regular Plans: Platforms that sell Regular Plans earn a trail commission from the AMC every year — typically 0.5% to 1% of your invested amount. When they say the app is free, this commission is how they actually get paid.

Advisory Fees: Some SEBI-registered investment advisors (RIAs) charge a flat annual fee (₹5,000 to ₹25,000/year) or a percentage of your portfolio (0.5% to 1% per year) for personalised portfolio management. This is not inherently wrong — good advisors can add value — but you must confirm whether the fee is justified by the service you receive.

PMS-Style Platform Charges: Premium portfolio management services and certain robo-advisory platforms charge annual management fees of 0.5% to 2.5% of your invested corpus. On a ₹50 lakh portfolio, that is ₹25,000 to ₹1,25,000 per year — every year.

My honest take: If you are investing purely in index funds and direct plans with a long-term horizon, you do not need to pay any advisory or platform fee whatsoever. Buy direct, stay invested, review annually. It is that simple — and you save every single rupee that would otherwise go to intermediaries.

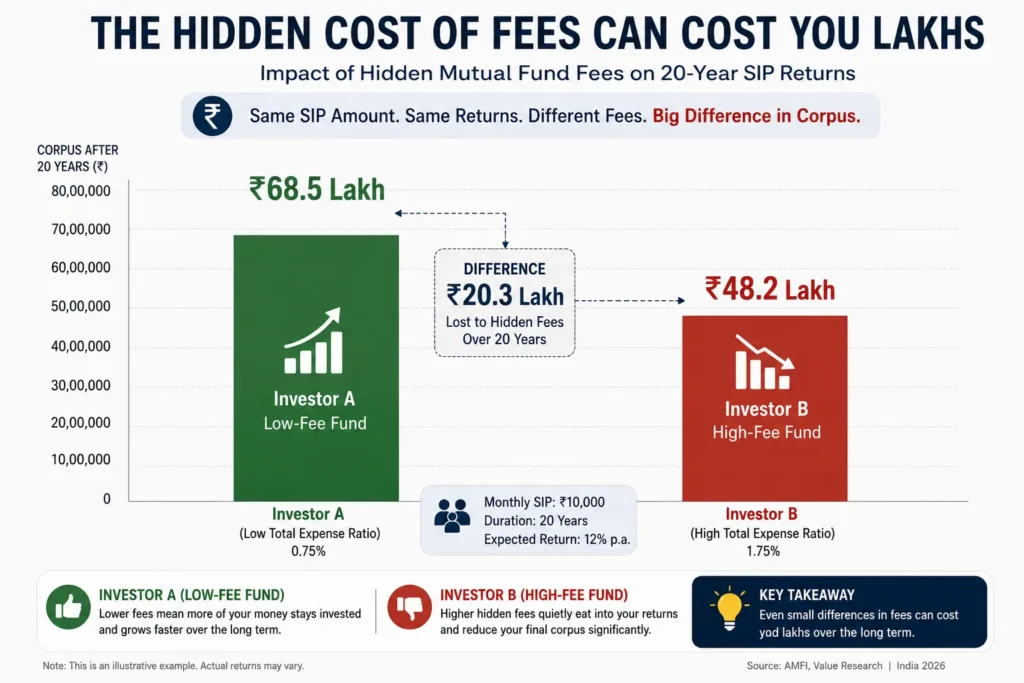

Real Example — How Hidden Mutual Fund Fees Destroy Wealth Over 20 Years

Let me bring all of this together with one concrete, realistic example.

Scenario: Two investors, ₹5,000 monthly SIP, 20 years

| Investor A (Smart) | Investor B (Unaware) | |

|---|---|---|

| Plan | Direct Plan | Regular Plan |

| Fund Type | Index Fund | Active Fund |

| Gross Return | 13% | 13% |

| Expense Ratio | 0.20% | 1.80% |

| Net Return | 12.80% | 11.20% |

| Exit Discipline | Held for full term | Exited early twice (paid exit load) |

| Tax Strategy | Growth, held 1yr+ | IDCW option (taxed at slab) |

| Final Corpus | ~₹68.5 lakh | ~₹48.2 lakh |

| Difference | ₹20.3 lakh more | — |

₹20.3 lakh difference. On the exact same monthly investment. Over the same 20-year period.

That gap represents the cumulative damage of hidden mutual fund fees — expense ratio, regular plan commission, exit load, and suboptimal tax choices — compounding quietly against Investor B’s wealth for two decades.

How to Avoid Hidden Mutual Fund Fees — 6 Practical Tips

Now that you know what the hidden mutual fund fees are, here is exactly what to do about each one:

Tip 1 — Always Buy Direct Plans Never buy through a bank, agent, or any platform that pushes Regular Plans. Use Zerodha Coin, MF Central, or the AMC’s own website to buy Direct Plans. This single change saves 0.5-1% every year — for life.

Tip 2 — Compare Expense Ratios Before Investing Before finalising any fund, check its Direct Plan expense ratio. For equity funds, aim for under 0.8%. For index funds, under 0.25% is ideal. Use Value Research Online to compare expense ratios across funds.

Tip 3 — Hold for More Than 1 Year Before Redeeming This avoids both the exit load (charged within 1 year) and the higher STCG tax (20%) versus LTCG (12.5%). Patience saves you real money.

Tip 4 — Choose the Growth Option, Not IDCW For all long-term SIP investments, always select the Growth option. The IDCW (Dividend) option triggers tax every time a dividend is paid — sometimes annually, sometimes quarterly — and that tax compounds against you over time.

Tip 5 — Use Index Funds for the Core of Your Portfolio Low expense ratio, zero distributor commission in Direct Plans, near-zero turnover costs, tax-efficient. A Nifty 50 or Nifty 500 index fund in Direct-Growth option is the most cost-efficient equity investment available to Indian retail investors.

Tip 6 — Read the Scheme Information Document Before Investing Every mutual fund publishes a Scheme Information Document (SID) and Key Information Memorandum (KIM) disclosing the expense ratio, exit load, and all charges. It takes 10 minutes to read — and could save you lakhs. Download it from the AMFI website at https://www.amfiindia.com.

Best Low-Cost Funds to Consider

| Fund Type | Example Funds | Approx. Expense Ratio (Direct) |

|---|---|---|

| Nifty 50 Index Fund | UTI Nifty 50, HDFC Nifty 50 | 0.10% – 0.20% |

| Nifty 500 Index Fund | Motilal Oswal Nifty 500 | 0.20% – 0.35% |

| Mid Cap Index Fund | Navi Nifty Midcap 150 | 0.12% – 0.20% |

| Low-Cost Active Flexi Cap | Parag Parikh Flexi Cap | 0.53% |

| ELSS Tax Saver | Mirae Asset ELSS | 0.50% – 0.70% |

The lower the expense ratio, the more of your returns you keep. It really is that simple.

iCommon Mistakes Investors Make

After tracking the hidden mutual fund fees story for years, these are the patterns I see repeatedly:

Buying Regular Plans Without Realising It: This is the single most common and costly mistake. Most first-time investors trust their bank’s relationship manager — who almost always recommends Regular Plans because that is what earns the bank a commission.

Ignoring Expense Ratio While Chasing Past Returns: A fund that returned 28% last year but charges 2% expense ratio is almost certainly going to disappoint over the next 5 years. High past returns attract attention. High expense ratios drain future returns.

Choosing IDCW Option for Monthly Income: Many investors like the feeling of receiving monthly “dividends.” In reality, IDCW payouts reduce your NAV by the dividend amount, trigger immediate tax at your slab rate, and interrupt compounding. It is a losing strategy for long-term wealth creation.

Redeeming Too Early: People get nervous during market corrections and withdraw their SIP investments — often just before a recovery. They pay exit load, trigger STCG tax, and miss the recovery. This is the most expensive emotional mistake in investing.

Not Reviewing Direct vs Regular Status Annually: Sometimes investors switch platforms and unknowingly land back in Regular Plans. Check your portfolio once a year to confirm you are still in Direct Plans.

Also Read

- Top 10 Mutual Funds for SIP to Invest in 2026 — Brilliant Picks

- Top 5 Mutual Funds for SIP to Invest in 2026 — Proven Outstanding Picks

FAQ — Hidden Mutual Fund Fees

Q1. Are mutual fund fees deducted monthly or annually?

Ans:- The expense ratio is technically deducted daily — it is factored into the daily NAV calculation. So while it is quoted as an annual percentage, the impact is spread across every single trading day. You never see it as a separate deduction; it is already accounted for in the NAV you see.

Q2. Which mutual fund has the lowest expense ratio in India?

Ans:- Index funds have the lowest expense ratios. Navi Nifty 50 Index Fund and UTI Nifty 50 Index Fund both offer expense ratios below 0.20% in their Direct Plans — making them among the most cost-efficient equity investments available to Indian retail investors.

Q3. Is a Direct Plan always better than a Regular Plan?

Ans:- For most self-directed investors — yes, absolutely. Direct Plans have 0.5% to 1% lower expense ratios than Regular Plans of the same fund. Over 15-20 years, this translates to lakhs of rupees in additional wealth. The only case where Regular Plans may be justified is if you have a genuinely active advisor who reviews and rebalances your portfolio regularly and whose advice adds clear value.

Q4. Can the expense ratio change over time?

Ans:- Yes. AMCs can revise expense ratios within the limits set by SEBI. SEBI caps maximum expense ratios based on fund size — as a fund grows larger, the maximum permissible expense ratio decreases. If a fund’s expense ratio increases, it must notify investors and SEBI. Always monitor your fund’s expense ratio annually.

Q5. What is a good expense ratio for a mutual fund in India?

Ans:- For index funds: anything below 0.25% is excellent. For actively managed equity funds in Direct Plans: 0.5% to 0.9% is reasonable. Above 1.2% in Direct Plans should be a red flag — that fund needs to consistently outperform its benchmark by more than 1.2% just to break even with an index fund.

Q6. Is LTCG tax applicable on all mutual funds?

Ans:- LTCG at 12.5% (above ₹1.25 lakh threshold) applies to equity and equity-oriented hybrid mutual funds held for more than 1 year. Debt mutual funds do not attract LTCG — instead, all gains are added to income and taxed at your applicable slab rate, regardless of how long you hold.

Q7. What is the exit load on most equity mutual funds?

Ans:- Most equity mutual funds charge 1% exit load on redemptions made within 1 year of each investment date. After 1 year, redemptions are typically exit-load-free. Always check the specific fund’s SID for exact exit load terms before investing.

Conclusion

Let me leave you with this thought.

Most investors spend hours researching which fund to invest in — comparing past returns, reading fund manager interviews, checking star ratings. Very few spend even 10 minutes checking what that fund is going to cost them over 20 years.

That is backwards.

The hidden mutual fund fees — expense ratio, regular plan commissions, exit load, STT, turnover costs, capital gains tax, and platform charges — collectively represent the single most controllable variable in your investment outcome. Markets are not in your control. Costs are.

Smart investors focus on both returns AND costs. They choose Direct Plans. They pick low-cost funds. They hold patiently to avoid exit loads and STCG tax. They choose Growth option over IDCW. These are not complicated decisions — but they can easily mean ₹15-20 lakh more in your final corpus.

Before you invest in any SIP today, spend 10 minutes checking the hidden charges first. Your future self will thank you for it.

Disclaimer: This article is published for educational and informational purposes only. Mutual fund investments are subject to market risks. Tax information is based on rules as of May 2026 and may change. Please consult a SEBI-registered investment advisor and a chartered accountant before making investment decisions.