Table of Contents

LIC Share Price Target 2026, 2027, 2028, 2029 & 2030

Let me be completely honest with you from the beginning.

When I first looked at the LIC share price target, I had mixed feelings. Here is a company that literally every Indian household knows — Life Insurance Corporation of India. Your parents have an LIC policy. Your grandparents had one too. LIC is practically woven into India’s financial DNA.

But does that make it a great stock? That is the real question.

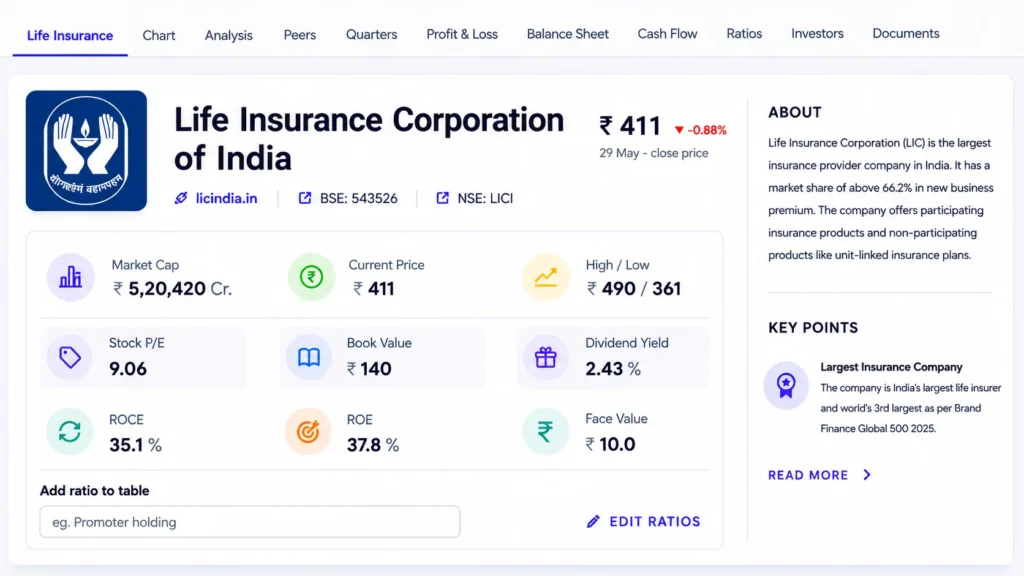

The current LIC share price is ₹411 as of May 29, 2026. It touched a 52-week high of ₹490 and came all the way down to ₹361. That is a big swing for a company of this size. So right now, a lot of retail investors are wondering — is this a buying opportunity or a value trap?

Let us figure that out together. Simply. Honestly.

| Year | Minimum Target | Average Target | Maximum Target |

|---|---|---|---|

| 2026 | ₹420 | ₹470 | ₹510 |

| 2027 | ₹480 | ₹550 | ₹620 |

| 2028 | ₹600 | ₹700 | ₹820 |

| 2029 | ₹750 | ₹900 | ₹1,050 |

| 2030 | ₹900 | ₹1,100 | ₹1,400 |

Company Background — What Does LIC Actually Do?

Imagine you are worried about what happens to your family if something bad happens to you. So you go to LIC, pay a small amount every month (called a premium), and LIC promises to give your family a big lump sum if the worst happens. That is life insurance in the simplest possible way.

Now multiply that by 300+ million policyholders across India. That is what LIC is.

Life Insurance Corporation of India was established in 1956 by the Government of India. It is not just a company — it is a national institution. The Indian government owns about 96.5% of LIC. It went public (IPO) in May 2022, which was the largest IPO in Indian stock market history.

How LIC Makes Money:

- Premiums: Customers pay premiums. LIC collects this money.

- Investments: LIC invests those premiums in stocks, bonds, and government securities. It is one of the largest institutional investors in the Indian stock market.

- Claim Settlements: When policyholders claim, LIC pays out. The difference between what it earns and what it pays is its profit.

LIC controls over 66.2% market share in new business premium in India. No private insurer comes close. HDFC Life, SBI Life, ICICI Pru Life — they are all fighting for the remaining 33.8%.

Think of LIC like the post office of insurance. It reaches every corner of India from Mumbai to a small village in Bihar. That reach is its biggest moat.

For more on LIC’s official products and policies, visit LIC India’s official website that is where you can check all current plans directly.

Current Share Price and Key Data From Screener

Based on Screener.in data as of May 29, 2026:

| Metric | Value |

|---|---|

| Current Price | ₹411 |

| 52-Week High / Low | ₹490 / ₹361 |

| Market Cap | ₹5,20,420 Crore |

| Stock P/E | 9.06 |

| Book Value | ₹140 |

| Dividend Yield | 2.43% |

| ROCE | 35.1% |

| ROE | 37.8% |

| Face Value | ₹10.00 |

| Listed On | BSE: 543526 / NSE: LICI |

The P/E of just 9.06 is genuinely interesting. Most insurance companies trade at 20-40x earnings. A P/E of 9 for a company with 66%+ market share and ₹5.2 lakh crore market cap is either a huge opportunity or the market is pricing in real concerns.

The ROE of 37.8% is outstanding. The ROCE of 35.1% is equally impressive. These numbers tell you that LIC is genuinely efficient at turning shareholder capital into profit.

The dividend yield of 2.43% is also decent — meaning if you invest ₹1 lakh in LIC, you get roughly ₹2,430 every year just in dividends, without selling a single share.

LIC Quarterly Results — What the Numbers Say

Looking at the quarterly results data from Screener, here is what stands out:

| Metric | Mar 2025 | Jun 2025 | Sep 2025 | Dec 2025 | Mar 2026 |

|---|---|---|---|---|---|

| Sales (₹ Cr) | 2,43,134 | 2,24,671 | 2,41,524 | 2,35,954 | 2,76,744 |

| Operating Profit (₹ Cr) | 21,514 | 10,474 | 9,492 | 12,366 | 11,222 |

| Net Profit (₹ Cr) | 19,039 | 10,955 | 10,096 | 12,908 | 23,467 |

| EPS (₹) | 15.05 | 8.66 | 7.98 | 10.22 | 18.55 |

The March 2026 quarter is the standout here. Net profit of ₹23,467 crore — the highest in the last several quarters. EPS jumped to ₹18.55, which is very strong.

Full Year FY26 (Annual) Highlights:

From the Profit & Loss data:

- Sales grew from ₹8,89,970 crore (FY25) to ₹9,77,772 crore (FY26) — about 10% growth

- Net Profit jumped from ₹48,320 crore (FY25) to ₹57,453 crore (FY26) — nearly 19% growth

- EPS grew from ₹38.20 to ₹45.42

Compounded Growth Rates (from Screener):

| Period | Sales Growth | Profit Growth | Stock Price CAGR | ROE |

|---|---|---|---|---|

| 5 Years | 7% | 81% | — | 52% |

| 3 Years | 8% | 17% | 11% | 46% |

| TTM | 10% | 20% | -13% | 38% |

That 5-year profit CAGR of 81% is spectacular. Sales growth is slow (7%) but profits have exploded — this means LIC has been getting much more efficient and profitable even without massive revenue growth.

LIC Share Price Target 2027

For 2027, the LIC share price target depends on a few key things:

- Whether profit growth continues at 15-20% annually

- Whether VNB (Value of New Business) margins improve from insurance-specific operations

- Whether the government reduces its stake (which could trigger a re-rating)

| Scenario | Target Price |

|---|---|

| Conservative (slow growth) | ₹480 – ₹520 |

| Base Case (current trajectory) | ₹530 – ₹600 |

| Optimistic (re-rating + growth) | ₹620 – ₹680 |

My honest view: LIC at ₹411 with an EPS of ₹45.42 means it is trading at just 9x earnings. If the market starts valuing it closer to 12x — which is still very conservative for an insurance company — the stock naturally reaches ₹545. A 2027 target of ₹550-₹600 is a reasonable base case.

For example, if you invest ₹1 lakh in LIC today at ₹411 and the stock reaches ₹560 by 2027, your investment becomes ₹1,36,252 — a 36% return in roughly 18 months. Plus you collect dividends along the way.

LIC Share Price Target 2028

By 2028, LIC’s story should become clearer. A few things that could drive the price higher:

- Continued growth in new business premiums from Tier 2 and Tier 3 cities

- Government potentially selling more stake through OFS (which brings in more institutional and FII investors)

- Digital transformation — LIC has been investing in technology to compete with private insurers

- Expansion into health insurance and pension products

| Scenario | Target Price |

|---|---|

| Conservative | ₹600 – ₹700 |

| Base Case | ₹700 – ₹820 |

| Optimistic | ₹850 – ₹950 |

If EPS grows at even 15% annually from ₹45.42 today, by FY28 EPS should reach approximately ₹60. At 12-13x P/E, that gives a price range of ₹720-₹780. Completely reasonable.

LIC Share Price Target 2029

By 2029, India’s insurance penetration story becomes even more powerful. Today, India’s life insurance penetration is around 3.2% of GDP. The global average is close to 7%. That gap will close over the next decade — and LIC sits right in the middle of that growth story.

| Scenario | Target Price |

|---|---|

| Conservative | ₹750 – ₹850 |

| Base Case | ₹880 – ₹1,000 |

| Optimistic | ₹1,050 – ₹1,200 |

If the P/E re-rating happens — which many analysts expect as FII participation increases — LIC at 15x earnings by 2029 is not unrealistic. That could put the stock at ₹1,000+.

LIC Share Price Target 2030

The 2030 targets are the most exciting — and also the most uncertain.

By 2030, if India’s economy reaches $5 trillion (which is the government’s stated target), insurance premiums will grow significantly. LIC, with its unmatched distribution network of 13+ lakh agents across India, is the best-positioned company to capture that growth.

| Scenario | Target Price |

|---|---|

| Conservative | ₹900 – ₹1,000 |

| Base Case | ₹1,050 – ₹1,200 |

| Optimistic | ₹1,300 – ₹1,500 |

Some algorithm-based target models suggest ₹1,400+ by 2030. That is aggressive but not impossible if earnings grow consistently and valuations normalise.

Full Target Summary:

| Year | Conservative | Base Case | Optimistic |

|---|---|---|---|

| 2027 | ₹480 – ₹520 | ₹530 – ₹600 | ₹620 – ₹680 |

| 2028 | ₹600 – ₹700 | ₹700 – ₹820 | ₹850 – ₹950 |

| 2029 | ₹750 – ₹850 | ₹880 – ₹1,000 | ₹1,050 – ₹1,200 |

| 2030 | ₹900 – ₹1,000 | ₹1,050 – ₹1,200 | ₹1,300 – ₹1,500 |

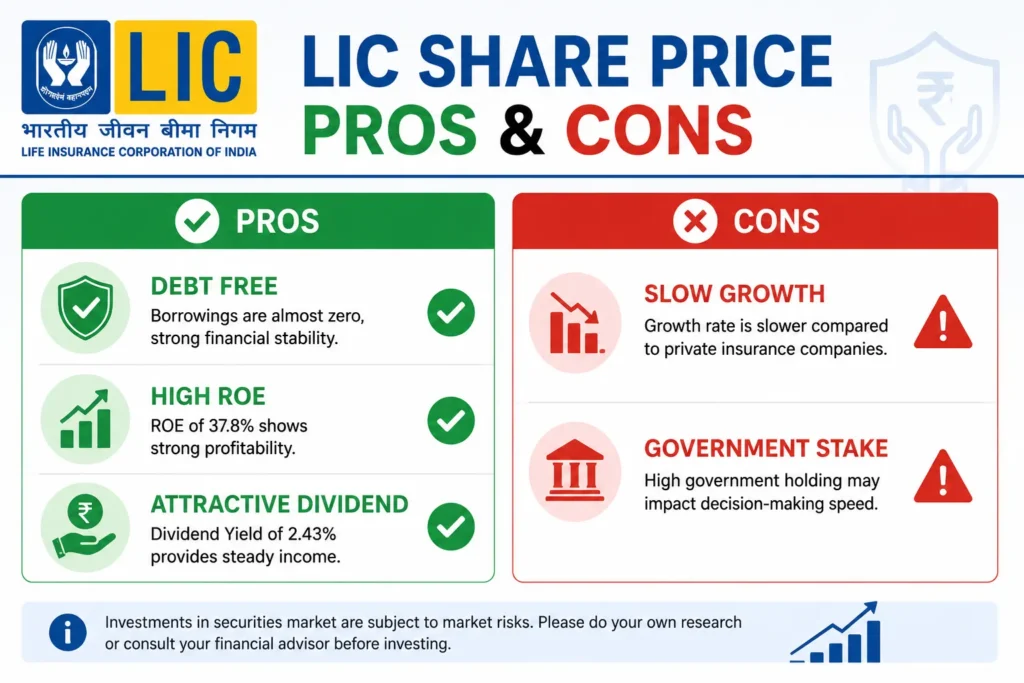

Pros of LIC Share — The Good Stuff

From the Screener data and quarterly results, here are the genuine positives:

1. Company Is Almost Debt Free This is huge. Most companies borrow money to run their business. LIC’s balance sheet shows borrowings of just ₹1 crore in FY26 against total assets of nearly ₹60 lakh crore. That is essentially zero debt. No debt means no interest burden — profits flow more freely to shareholders.

2. Excellent ROE Track Record — 3 Year ROE of 45.5% A 3-year ROE of 45.5% means for every ₹100 of your money sitting in the company, LIC generates ₹45.5 in profit annually. That is exceptional efficiency. Most banking and insurance companies would be happy with 15-18%.

3. Monopoly-Like Market Position 66.2% market share in new business premium. No private insurer has been able to meaningfully eat into LIC’s dominance despite 20+ years of competition.

4. Massive Agent Network Over 13 lakh agents reach every district, every town, every village. Building a network like this would take decades for any competitor. It is LIC’s biggest invisible asset.

5. Decent Dividend Yield of 2.43% Unlike most growth stocks that pay zero dividend, LIC pays you 2.43% per year just to hold the stock. That is better than many savings accounts.

6. Strong Profit Growth — 81% CAGR Over 5 Years Yes, you read that right. Even though sales grew slowly at 7%, profits have compounded at 81% over 5 years. This is because LIC has been cleaning up its investment book and improving operational efficiency significantly.

Cons and Risks — Things That Could Go Wrong

I always believe in being honest about the risks. Here is what concerns me:

1. Slow Sales Growth (Only 7% Over 5 Years) The profit growth is impressive, but sales are only growing at 7% annually. If top-line growth does not accelerate, eventually profit growth will slow down too. Private competitors are growing their premium income at 20-25% annually.

2. Tax Rate Seems Low Screener flags this as a concern — and it is worth paying attention to. In the most recent quarter (Mar 2026), the tax rate showed as -63%, which means LIC actually got a tax credit rather than paying tax. This kind of irregularity can distort profit numbers and may not repeat in future quarters.

3. Market Share Erosion Risk While LIC’s dominance is real today, private players like HDFC Life, SBI Life, and ICICI Pru are consistently growing faster. If this trend continues for another decade, LIC’s 66% could slowly become 55%, then 50%. That gradual erosion is a long-term concern.

4. Government Overhang The Indian government owns 96.5% of LIC. Any large stake sale by the government to meet fiscal targets could put pressure on the stock price short-term. This is a risk that does not apply to private sector companies.

5. Investment Portfolio Concentration LIC is one of the largest shareholders in dozens of Indian companies. If the stock market goes through a prolonged bear phase, LIC’s investment book takes a hit — which directly impacts its profits.

6. Bureaucratic Culture Compared to nimble private insurers, LIC is slower to innovate in digital products, online policy issuance, and customer experience. The private sector is eating its lunch in the high-value, urban customer segment.

Should You Invest in LIC Share?

Here is my honest answer.

If you are a patient, long-term investor (3-5 year horizon): LIC at ₹411 with a P/E of 9 and ROE of 37.8% is genuinely cheap for what you are getting. The profit growth has been spectacular. The dividend provides some passive income while you wait. If valuations normalise even modestly — from 9x to 12-13x — the stock could be 35-50% higher without any additional earnings growth.

If you want quick gains: This is probably not your stock. LIC has been drifting sideways and downward for most of the last year. The 52-week price is ₹490 to ₹361 a wide range. Short-term traders have not been rewarded.

If government ownership makes you nervous: That is a completely valid concern. LIC is partly a policy tool, not purely a profit-maximising company. The government uses LIC’s investment book to support PSU stocks and government bond markets. This sometimes means LIC does not act purely in shareholders’ interests.

Think of LIC like a giant mango orchard that someone else tends for you. The orchard (the business) is massive and incredibly productive. You own a small piece of it. The main gardener (the government) sometimes uses some of the mangoes for other purposes (policy goals). But overall, the orchard produces a lot of fruit — and you get some of it every year in the form of dividends and capital gains.

Key things to track every quarter:

- Is profit growth sustaining at 15-20%?

- Is market share holding above 60%?

- What is happening with the tax rate (any one-time items)?

- Is the government announcing any stake sale?

For tracking LIC’s financials in detail, check Screener.in’s LIC page — it is the best free tool for Indian stock fundamentals. You can also follow LIC’s investor relations page at licindia.in for official quarterly results.

Also Read

- KPI Green Energy Share Price Target 2026-2030 — Full Analysis

- How to Invest in Share Market for Beginners in India — Step by Step Guide 2026

- Top 5 Best Indian Stocks to Buy in 2026 for Long-Term Wealth Creation

FAQ

Q1. What is the LIC share price target for 2027?

Ans:- The LIC share price target for 2027 is expected to be around ₹530 to ₹600 in normal market conditions. If profit growth continues and valuations improve, the stock could reach ₹620 to ₹680.

Q2. What is the LIC share price target for 2028?

Ans:- The LIC share price target for 2028 is estimated between ₹700 and ₹820 in the base case. If the P/E re-rating happens, the stock may cross ₹900 by FY28.

Q3. What is the LIC share price target for 2030?

Ans:- The LIC share price target for 2030 could range from ₹1,050 to ₹1,200 in the base scenario. In a highly positive case with P/E re-rating, the stock may reach ₹1,400-₹1,500.

Q4. Is LIC a good long-term investment?

Ans:- LIC looks interesting for long-term investors because of its near-monopoly position, low valuation (P/E of 9), excellent ROE of 37.8%, and 2.43% dividend yield. However, slow sales growth and government ownership are genuine concerns to keep in mind.

Q5. What is the current LIC share price?

Ans:- As of May 29, 2026, the LIC share price is ₹411 on NSE (ticker: LICI) and BSE (543526). The 52-week high is ₹490 and the 52-week low is ₹361.

Q6. Does LIC pay a good dividend?

Ans:- LIC has a dividend yield of 2.43%, which is decent for an Indian stock. It is better than most growth stocks. The dividend payout has been consistent since its listing in 2022.

Q7. Why is LIC’s P/E so low?

Ans:- LIC trades at a P/E of around 9 because the market has concerns about slow sales growth, government ownership, and competition from private insurers. Many analysts believe this low valuation is an opportunity — but it requires patience for re-rating to happen.

Q8. What are the main risks in LIC’s share price target projections?

Ans:- The main risks are slow revenue growth, gradual market share loss to private insurers, government stake sale overhang, dependence on investment income, and potential policy changes affecting the insurance sector.

Disclaimer: This article is for educational and informational purposes only. Share price targets mentioned are based on publicly available data from Screener.in, analyst reports, and author opinion. They do not constitute investment advice. Stock markets are subject to risks. Please consult a SEBI-registered investment advisor before making any investment decision. Past performance is not a guarantee of future returns.