Table of Contents

Adani Power Share Price Target 2026 to 2030

Let me be totally straight with you from the start.

When I first looked at the Adani Power share price target, I had a very specific reaction this stock has already done something extraordinary. The 1-year stock price CAGR is 124%. The 5-year CAGR is 66%. The 10-year CAGR is 45%.

Think about that for a second. If you had put ₹1 lakh in Adani Power ten years ago, it would be worth over ₹35 lakh today.

But here is the real question can that kind of return continue? Or has the easy money already been made?

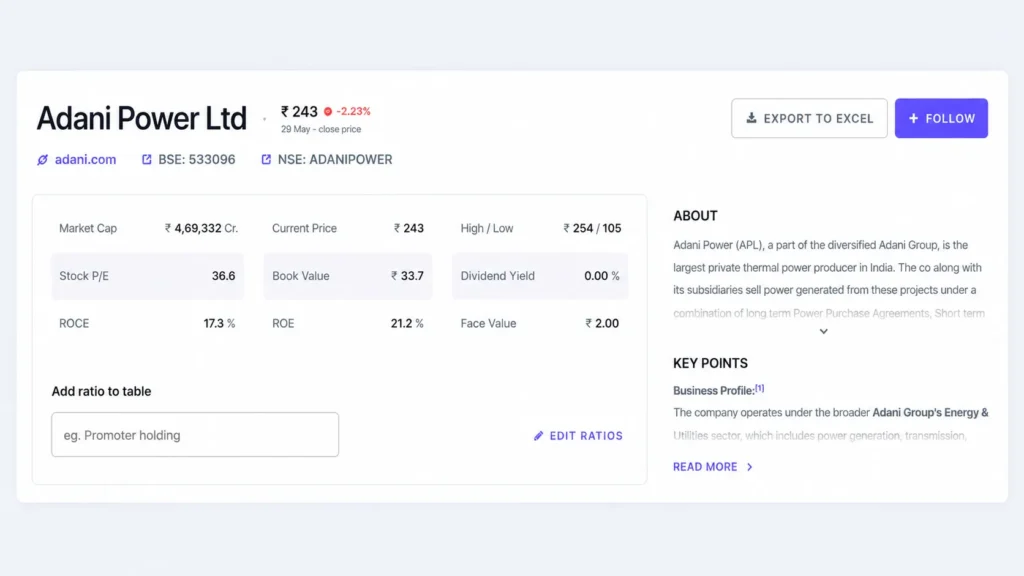

The current Adani Power share price is ₹243 as of May 29, 2026. It touched a 52-week high of ₹254 and a low of ₹105. That is a stock that literally more than doubled in a single year and is now hovering near its highs.

So the question every investor is asking right now is what is the Adani Power share price target for 2027, 2028, 2029, and 2030? Is this still a buy? Or is the growth story priced in?

Let us break it down.

| Year | Minimum Target | Average Target | Maximum Target |

|---|---|---|---|

| 2026 | ₹220 | ₹260 | ₹300 |

| 2027 | ₹280 | ₹340 | ₹410 |

| 2028 | ₹380 | ₹470 | ₹560 |

| 2029 | ₹480 | ₹600 | ₹750 |

| 2030 | ₹600 | ₹800 | ₹1,050 |

Adani Power Company Background

Imagine a huge coal power plant somewhere in Gujarat or Rajasthan. Giant chimneys, massive turbines, thousands of tonnes of coal burning every day to produce electricity. That electricity then travels through power lines to factories, cities, and homes across India.

That is what Adani Power does at a massive scale.

Adani Power Limited (APL) is part of the diversified Adani Group. It is the largest private thermal power producer in India, accounting for 7.3% of India’s domestic coal-based power generation capacity. It is listed on BSE (533096) and NSE (ADANIPOWER).

The company operates power plants across multiple states Gujarat, Rajasthan, Maharashtra, Karnataka, Chhattisgarh, and Madhya Pradesh. It sells this electricity through three routes:

- Long-term Power Purchase Agreements (PPA): Fixed contracts with electricity boards like stable rental income.

- Short-term PPA: Shorter contracts, a bit more flexible.

- Merchant basis: Selling in the open market at spot prices higher risk but potentially higher reward.

The company also operates under the broader Adani Group’s Energy & Utility portfolio, which spans power generation, transmission, distribution, renewable energy, and international power exports.

Think of Adani Power like a giant electricity factory. It makes the electricity. Grid companies carry it. End users consume it. Adani Power sits at the very beginning of that chain — and India needs more and more electricity every single year.

For official information on Adani Power’s projects and operations, you can visit Adani’s official website directly.

Current Share Price and Key Data From Screener

Based on Screener.in data as of May 29, 2026:

| Metric | Value |

|---|---|

| Current Price | ₹243 |

| 52-Week High / Low | ₹254 / ₹105 |

| Market Cap | ₹4,69,332 Crore |

| Stock P/E | 36.6 |

| Book Value | ₹33.7 |

| Dividend Yield | 0.00% |

| ROCE | 17.3% |

| ROE | 21.2% |

| Face Value | ₹2.00 |

| Listed On | BSE: 533096 / NSE: ADANIPOWER |

The P/E of 36.6 is high but not unreasonable for the largest private power producer in India. Compare this to peers: Tata Power trades at 35.4x, Torrent Power at 29.6x. So Adani Power is actually in line with the sector.

The stock is trading at 7.23x its book value of ₹33.7. This means the market is paying a hefty premium for Adani Power’s assets a sign of confidence but also a risk if growth slows.

The zero dividend is something income investors need to know upfront. Adani Power has never paid a dividend not once in its listed history. This is a pure growth stock. You invest for capital appreciation, not passive income.

The ROE of 21.2% and 3-year ROE of 31.8% are genuinely strong numbers. The company is generating solid returns on shareholder capital.

For the latest live data, check Screener.in’s Adani Power page it is the best free tool for tracking Indian stock fundamentals.Adani Power Quarterly Results — The Numbers Behind the Story

Here is the quarterly picture data:

| Quarter | Sales (₹ Cr) | Operating Profit (₹ Cr) | Net Profit (₹ Cr) | EPS (₹) |

|---|---|---|---|---|

| Mar 2025 | 14,237 | 4,813 | 2,599 | 1.37 |

| Jun 2025 | 14,109 | 5,685 | 3,305 | 1.76 |

| Sep 2025 | 13,457 | 5,150 | 2,906 | 1.53 |

| Dec 2025 | 12,451 | 4,238 | 2,488 | 1.29 |

| Mar 2026 | 14,223 | 4,732 | 4,271 | 2.08 |

The March 2026 quarter is the standout net profit of ₹4,271 crore, up a massive 52.34% year-on-year. Revenue held flat at ₹14,223 crore, but profit jumped sharply showing margin expansion at work.

Full Year FY26 Annual Results:

| Metric | FY25 | FY26 | Change |

|---|---|---|---|

| Sales (₹ Cr) | 56,203 | 54,241 | -3% |

| Operating Profit (₹ Cr) | 21,418 | 19,806 | -8% |

| Net Profit (₹ Cr) | 12,750 | 12,971 | +2% |

| EPS (₹) | 6.71 | 6.66 | Flat |

The FY26 full-year numbers are a bit mixed. Sales actually declined 3% and operating profit dropped 8%. Net profit barely grew. But the Q4 FY26 quarter was very strong which gives some confidence that the second half of FY26 was recovering well.

Compounded Growth :

| Period | Sales Growth | Profit Growth | Stock Price CAGR | ROE |

|---|---|---|---|---|

| 10 Years | 8% | 37% | 45% | 27% |

| 5 Years | 16% | 59% | 66% | 33% |

| 3 Years | 12% | 6% | 69% | 32% |

| TTM | -3% | -1% | 124% | 21% |

That last row is interesting TTM (trailing twelve months) sales and profit are both slightly negative, yet the stock price CAGR over 1 year is 124%. This tells you the stock ran significantly ahead of fundamentals in the last year. The market was pricing in future growth which means the current valuation has high expectations baked in.

Adani Power Share Price Target 2027

For 2027, the Adani Power share price target depends on:

- Whether Q4 FY26’s strong profit momentum continues into FY27

- Capacity utilisation improvement at existing plants

- New capacity additions — CWIP (Capital Work in Progress) jumped to ₹35,053 crore in FY26 from ₹12,104 crore in FY25. This massive investment should start generating revenue by FY27-28.

- India’s growing electricity demand peak demand crossed 250 GW in FY26

| Scenario | Target Price |

|---|---|

| Conservative (earnings flat) | ₹220 – ₹260 |

| Base Case (10-15% earnings growth) | ₹280 – ₹340 |

| Optimistic (strong capacity addition) | ₹380 – ₹420 |

At ₹243 with EPS of ₹6.66, the stock is at 36.6x earnings already pricing in significant growth. For the stock to re-rate higher by 2027, earnings need to actually grow. The strong CWIP investments suggest FY27-28 could see a meaningful jump in revenue and profit as new plants come online. A base case target of ₹300-₹340 by end of 2027 is reasonable if capacity additions deliver.

Example: If you invest ₹1 lakh today at ₹243 and the stock reaches ₹320 by 2027, your investment becomes ₹1,31,687 — a 31.7% return in 18 months.

Adani Power Share Price Target 2028

By 2028, the CWIP of ₹35,053 crore should start converting into productive assets. This is the single most important number to track for Adani Power’s future.

When capital work in progress becomes fixed assets, it starts generating revenue. Adani Power is clearly in a massive expansion phase and 2028 is when that expansion should start showing up in earnings.

Additionally, India’s power demand is expected to grow at 6-7% annually. With the government’s push for industrial growth and data centres requiring uninterrupted power, thermal power remains critical even as renewables grow.

| Scenario | Target Price |

|---|---|

| Conservative | ₹340 – ₹400 |

| Base Case | ₹430 – ₹500 |

| Optimistic | ₹520 – ₹600 |

If EPS recovers to ₹10-12 by FY28 (from ₹6.66 today) as new capacity comes online, and the market values it at 35-40x earnings, the stock naturally reaches ₹350-₹480. A base case of ₹450-₹500 by 2028 seems achievable.

Adani Power Share Price Target 2029

By 2029, Adani Power’s story is about scale. The company is building capacity aggressively — total assets grew from ₹92,009 crore in FY24 to ₹1,42,280 crore in FY26, a jump of over 54% in just two years. That kind of asset growth, when it translates to earnings, can be powerful.

India’s electricity consumption is expected to double by 2030 compared to 2022 levels. Thermal power will remain a significant part of that mix especially for baseline load that solar and wind cannot always guarantee.

| Scenario | Target Price |

|---|---|

| Conservative | ₹430 – ₹500 |

| Base Case | ₹540 – ₹650 |

| Optimistic | ₹700 – ₹800 |

The promoter holding has stabilised at 74.96% for the last several quarters which is a positive sign. FII holding at 11.73% and DII holding growing from 0.04% (Jun 2023) to 3.69% (Mar 2026) shows increasing institutional confidence in the stock.

Adani Power Share Price Target 2030

The 2030 picture is the most exciting and the most uncertain. A lot can change in 4 years.

What we know for 2030:

- India targets 500 GW of renewable energy but thermal will still be needed for baseload

- India’s power demand is forecast to reach 400+ GW by 2030

- Adani Group has stated ambitions for international power exports

- The CWIP investments being made today will be fully productive by 2030

| Scenario | Target Price |

|---|---|

| Conservative | ₹550 – ₹650 |

| Base Case | ₹700 – ₹850 |

| Optimistic | ₹900 – ₹1,100 |

Full Target Summary:

| Year | Conservative | Base Case | Optimistic |

|---|---|---|---|

| 2027 | ₹220 – ₹260 | ₹280 – ₹340 | ₹380 – ₹420 |

| 2028 | ₹340 – ₹400 | ₹430 – ₹500 | ₹520 – ₹600 |

| 2029 | ₹430 – ₹500 | ₹540 – ₹650 | ₹700 – ₹800 |

| 2030 | ₹550 – ₹650 | ₹700 – ₹850 | ₹900 – ₹1,100 |

Pros of Adani Power Share

1. Strong ROE Track Record — 3 Years ROE of 31.8% This is the standout positive from Screener’s own analysis. A 3-year ROE of 31.8% means Adani Power has been generating exceptional returns on shareholder equity. Most power companies struggle to cross 15-20% ROE.

2. Largest Private Thermal Power Producer in India 7.3% of India’s domestic coal-based power generation that is a dominant position. Building this kind of capacity takes decades and billions in capital. It is a genuine competitive moat.

3. Explosive Stock Price Performance 10-year stock CAGR of 45%, 5-year CAGR of 66%, 1-year CAGR of 124%. If you have been a shareholder, you have been rewarded very well.

4. Massive Capacity Expansion Underway CWIP jumped from ₹12,104 crore (FY25) to ₹35,053 crore (FY26). This means Adani Power is spending aggressively on new capacity — which should translate to higher revenue and profit by FY27-28.

5. Strong Cash Generation Cash from operating activity was ₹20,514 crore in FY26. The company generates strong operating cash flow — a sign of a healthy core business even if profits look lumpy quarter to quarter.

6. Growing Institutional Confidence DII holding has grown from near zero (0.04% in Jun 2023) to 3.69% in Mar 2026. Domestic mutual funds and institutions are steadily buying — that is a positive signal.

7. Part of Adani Group’s Energy Ecosystem Being part of Adani’s broader energy group — which includes transmission, distribution, and renewables — gives Adani Power strategic advantages in power evacuation, land access, and project financing.

Cons and Risks — What Could Go Wrong

1. Stock Trading at 7.23x Book Value This is the first red flag Screener flags. Paying ₹7.23 for every ₹1 of book value means you are paying a very high premium. If earnings growth disappoints, the stock could correct sharply to normalise valuation.

2. Zero Dividend — Never Paid Once Not a single rupee in dividend in its entire listed history. For income investors, this stock offers nothing while you wait. You are entirely dependent on price appreciation.

3. Company Might Be Capitalising Interest Costs Screener specifically flags this as a concern. Capitalising interest means instead of showing interest as an expense (which reduces profit), the company adds it to the cost of assets under construction. This can make current profits look better than they really are. It is a legitimate concern worth tracking.

4. Debt Has Been Rising Borrowings jumped from ₹34,862 crore (FY24) to ₹54,670 crore (FY26) an increase of nearly ₹20,000 crore in just two years. This is being used to fund the massive CWIP expansion. While growth-oriented debt can be justified, rising debt also means higher interest obligations. Interest cost was ₹3,367 crore in FY26.

5. FY26 Revenue Actually Declined Full year FY26 sales were ₹54,241 crore lower than FY25’s ₹56,203 crore. A 3% revenue decline for the full year is not what you want to see in a growth stock. The Q4 FY26 recovery helps, but the full year picture is mixed.

6. Adani Group Conglomerate Risk This is unique to Adani Group stocks. Any negative news related to the broader Adani Group regulatory issues, financing concerns, or geopolitical headwinds can drag down all Adani stocks including Adani Power, even if the individual company is doing fine. This happened sharply in early 2023 during the Hindenburg report episode.

7. Coal Dependency in a Decarbonising World Long term and I mean 10-20 year horizon thermal power based on coal faces structural headwinds. ESG investing trends, carbon taxes, and global pressure on coal assets could limit how much premium the market assigns to Adani Power’s valuation in the long run.

Peer Comparison — How Does Adani Power Stack Up?

| Company | CMP (₹) | P/E | Market Cap (₹ Cr) | Div Yield | Q4 Net Profit (₹ Cr) | ROCE% |

|---|---|---|---|---|---|---|

| Adani Power | 243 | 36.6 | 4,69,332 | 0% | 4,271 | 17.3 |

| Tata Power | 420 | 35.4 | 1,34,444 | 0.59% | 1,416 | 10.5 |

| Torrent Power | 1,420 | 29.6 | 71,569 | 1.34% | 331 | 14.0 |

| CESC | 182 | 15.7 | 24,137 | 3.30% | 459 | 10.6 |

A few key observations:

Adani Power has by far the highest market cap and the highest quarterly net profit (₹4,271 crore vs Tata Power’s ₹1,416 crore). Its profitability dominance is clear.

However, Adani Power’s ROCE of 17.3% is the lowest in this comparison group in terms of capital efficiency. Tata Power at 10.5% is also not great, but CESC at 10.6% pays 3.3% dividend too.

For income investors, Torrent Power (1.34% dividend) or CESC (3.3% dividend) might be more suitable. For pure growth, Adani Power leads the pack.

Should You Invest in Adani Power Share?

If you are a long-term growth investor (3-5 years): The expansion story is real. ₹35,053 crore in CWIP means significant new capacity is coming. If India’s electricity demand continues growing at 6-7% annually, Adani Power is in the right place. The stock has rewarded long-term holders extraordinarily well.

If you are looking for value: This is not the stock. At 7.23x book value and 36.6x earnings with flat FY26 revenue, the stock is pricing in a lot of future growth. There is limited margin of safety at the current price.

If you are an income investor: Please look elsewhere. Zero dividend, zero history of income sharing with shareholders. This is a 100% capital appreciation play.

If Adani Group news makes you nervous: That is a completely valid concern. Adani Group stocks tend to move together on group-level news. If that volatility keeps you up at night, it may not be the right investment for your temperament.

Think of Adani Power like a massive power grid expansion project. The contractor (Adani Power) is investing hugely upfront new plants, new equipment, new transmission linkages. For the next 1-2 years, costs are high and profits may be lumpy. But by 2028-2030, if all those plants come online and India’s electricity demand keeps growing, the revenue and profits should be significantly higher than today.

The risk is construction delays, cost overruns, regulatory issues, or a slowdown in electricity demand. The reward is being part of India’s foundational infrastructure build-out.

Key things to track every quarter:

- Is CWIP converting to fixed assets (i.e., are new plants being commissioned)?

- Is operating profit margin holding above 35-38%?

- Is promoter pledging data available and stable?

- Are there any Adani Group-level regulatory developments?

Also check India’s electricity sector policies at Ministry of Power India’s official website government decisions on tariffs, coal linkages, and capacity auctions directly affect Adani Power’s earnings.

Also Read

- LIC Share Price Target 2026 to 2030 — Honest Analysis With Real Data

- KPI Green Energy Share Price Target 2026 to 2030 — Full Analysis

- Top 5 Best Indian Stocks to Buy in 2026 for Long-Term Wealth Creation

- Defence Stocks in India 2026: Best Defence Shares to Watch, Buy & Track

FAQ — Adani Power Share Price Target

Q1. What is the Adani Power share price target for 2027?

Ans:- The Adani Power share price target for 2027 is expected to be around ₹280 to ₹340 in normal market conditions. If new capacity additions boost earnings significantly, the stock may reach ₹380 to ₹420 by end of 2027.

Q2. What is the Adani Power share price target for 2028?

Ans:- The Adani Power share price target for 2028 is estimated between ₹430 and ₹500 in the base case. If the current CWIP investments start generating strong revenue, the stock could push toward ₹560 to ₹600.

Q3. What is the Adani Power share price target for 2030?

Ans:- The Adani Power share price target for 2030 ranges from ₹700 to ₹850 in the base scenario. In a highly optimistic case where India’s power demand surges and Adani Power executes all planned capacity additions, the stock may reach ₹900 to ₹1,100.

Q4. Is Adani Power a good long-term investment?

Ans:- Adani Power looks interesting for long-term growth investors because of its dominant market position, strong ROE track record, and massive capacity expansion underway. However, zero dividend, high valuation, rising debt, and Adani Group conglomerate risk are genuine concerns before investing.

Q5. What is the current Adani Power share price?

Ans:- As of May 29, 2026, the Adani Power share price is ₹243 on NSE (ADANIPOWER) and BSE (533096). The 52-week high is ₹254 and the 52-week low is ₹105.

Q6. Why did Adani Power stock go up 124% in one year?

Ans:- The stock rose sharply due to strong Q4 FY26 results (net profit up 52% YoY), India’s rising electricity demand, and the market re-rating Adani Power as a dominant private power producer. The broader Adani Group recovery post-2023 also helped sentiment.

Q7. Does Adani Power pay dividend?

Ans:- No. Adani Power has never paid a dividend the dividend payout has been 0% every year since listing. It is purely a capital appreciation stock.

Q8. What are the main risks in the Adani Power share price target projections?

Ans:- The main risks are high current valuation (7.23x book), rising debt levels, flat FY26 revenues, capitalisation of interest costs, Adani Group-level conglomerate risk, and long-term structural headwinds from decarbonisation and the global shift away from coal-based power.

Q9. What is Adani Power’s promoter holding?

Ans:- As of March 2026, promoter holding in Adani Power stands at 74.96% stable for the last several quarters. FII holding is 11.73% and DII holding has been growing steadily, reaching 3.69% in March 2026.

Q10. How does Adani Power compare with Tata Power?

Ans:- Adani Power has a much larger market cap (₹4.69 lakh crore vs Tata Power’s ₹1.34 lakh crore) and significantly higher quarterly profits (₹4,271 crore vs ₹1,416 crore). However, Tata Power pays a small dividend and has a stronger renewable energy portfolio, which may be more relevant for ESG-focused investors.

Disclaimer: I wrote this article only to share information and help you understand this stock better. The price targets I mentioned are based on publicly available data from Screener.in, I am not a SEBI-registered advisor. Please do not make any investment decision based only on what I have written here. Always consult a qualified financial advisor before investing. Stock markets carry risk and past performance never guarantees future results. Everything here is purely educational — your money, your responsibility. Invest wisely.